For years, housing advocates have sought tweaks to the Low Income Housing Tax Credit program that intend to bolster the number of affordable units produced each year.

Recently, those advocates succeeded in their efforts, as two essential changes were codified as part of the sprawling One Big Beautiful Bill Act (H.R. 1), signed into law early last month.

The first is important, and increases the annual amount of nine percent credits by 12 percent (indexed for inflation moving forward).

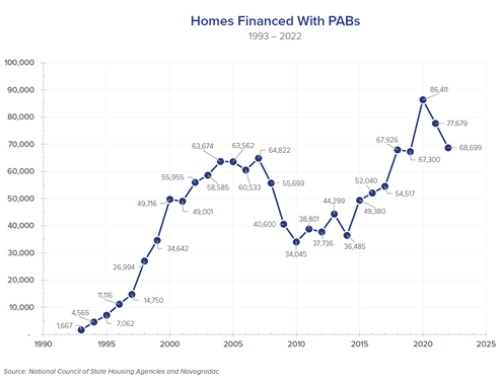

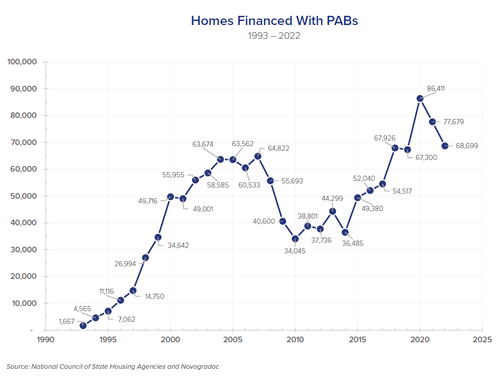

However, it is the other change to the LIHTC program that advocates say will have the most significant impact for housing in the near future: a reduction from 50 to 25 percent in the amount of tax-exempt private activity bonds (PABs) required to qualify for four percent credits.

“It’s exciting – this will be, we think, the biggest change to the four percent tax credit industry in the last 20 years,” says Kent Neumann, founding member at Tiber Hudson.

Many industry leaders see this as a positive and helpful change in the ongoing effort to build more housing. “Achieving the 25 percent bond financing threshold is a major victory that will enable a significant increase in the number of affordable units that are possible using the Housing Credit,” says James Tassos, deputy director of tax policy and strategic initiatives at the National Council of State Housing Agencies.

Introducing the 25 Percent Test

Known formerly as the “50 percent test,” this rule allowed properties, whose aggregate basis costs were funded by 50 percent or more via tax-exempt PABs, to claim tax credits outside of the allocating agency’s nine percent LIHTC volume cap. These tax credits are what today is known as the four percent LIHTC program.

In addition to unlocking funding via the LIHTC program, PABs also provide low-cost capital to a project by allowing developers to receive low-interest, tax-exempt loans from investors via bond proceeds. Known in the industry as “permanent supportable debt,” these loans are then paid back to investors over time, plus interest.

Thus, the 50 percent test has historically been the mechanism by which the four percent LIHTC program has functioned. Though there are no state or federal allocation limits to the four percent LIHTC program, the federal government can functionally limit the number of four percent LIHTC projects in any given year by tying these awards to tax-exempt PABs, since states are given an annual volume cap of tax-exempt PABs that they may allocate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}