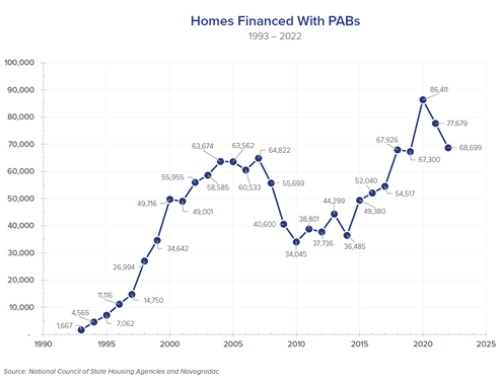

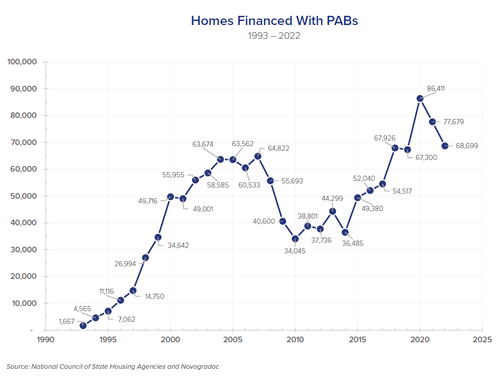

On January 1, 2026, the amount of tax-exempt Private Activity Bonds (PABs) required to qualify for the four percent Low Income Housing Tax Credit (LIHTC) will be lowered from 50 to 25 percent of a project’s aggregate basis (the “25 percent test”). Nationwide, state agencies have been busy gearing up for this rule change, which experts say may have profound effects on affordable multifamily housing production.

Already, states are developing industry-recommended allocation policies and turning to creative auxiliary strategies such as bond recycling to maximize program efficiency.

Advocates hope this change will significantly increase the number of units produced via the LIHTC program, as many states currently issue their maximum allowable PABs (which is known in the industry as being “oversubscribed”). According to some estimates, roughly half of the states in the country are currently oversubscribed.

A New Wave of Bond Capacity

The new 25 percent test will free up the availability of “new money” bond volume cap (i.e., the type of volume cap needed to qualify a project for four percent LIHTCs, as distinct from “recycled” volume cap, discussed below) in oversubscribed states, theoretically allowing more deals to qualify for four percent LIHTCs.

The long-advocated-for lowering of the 50 percent bond test was codified in the One Big Beautiful Bill Act (H.R. 1), signed into law in July of this year. The new reduced threshold will apply to deals placed in service after Jan. 1, 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}